7 Stark Realities Undermining the Municipal Bond Market’s Illusion of Stability

Municipal bonds, long touted as safe havens for conservative investors, are showing signs of fragility that demand more sober scrutiny. Despite a recent veneer of steadiness, underpinned by a subdued new-issue calendar in a holiday-shortened week, the market’s fundamentals betray underlying stress. Treasury yields have risen, pushing equity indices like the S&P 500 and Nasdaq to fresh record highs, but municipal bonds haven’t kept pace, exemplifying a disconnect that investors can no longer ignore. This divergence is troubling because it hints at shifting risk appetites, supply pressures, and valuation misalignments that could unsettle what’s been perceived as a rock-solid asset class.

The Overwhelming Surge in Supply

The sheer volume of municipal bond issuance is the most glaring warning sign. June 2025 is poised to be the largest monthly issuance since records have been kept, topping $50 billion. For the full year, projections have been ratcheted up dramatically, with BofA Securities now estimating $580 billion, up from an already ambitious $520 billion. This supply glut is far from benign—it exerts downward pressure on prices and forces yields higher, exacerbating the underperformance of tax-exempt munis this year. With redemptions and coupon payments barely keeping pace, there is a palpable risk that the market dynamic shifts unfavorably, particularly in the second half of the year when Barclays anticipates supply might contract 10%, but only relative to an unsustainably high baseline.

Market Technicals Mask a Brewing Storm

Common narratives suggest that muni bonds traditionally rebound during summertime months like July and August, buoyed by favorable supply-demand dynamics. However, the data show these past patterns are tenuous at best. Municipal-to-Treasury (MMD-UST) ratios, a key measure of relative value, have indeed compressed in July historically but also experienced sell-offs in August—timing that looks precarious given this year’s inflated issuance. While some strategists trumpet “good value” at current yield levels, this optimism smacks of complacency. The high issuance levels mean the market’s technicals are stretched thin. Any uptick in interest rates or change in investor sentiment could trigger disproportionate price declines.

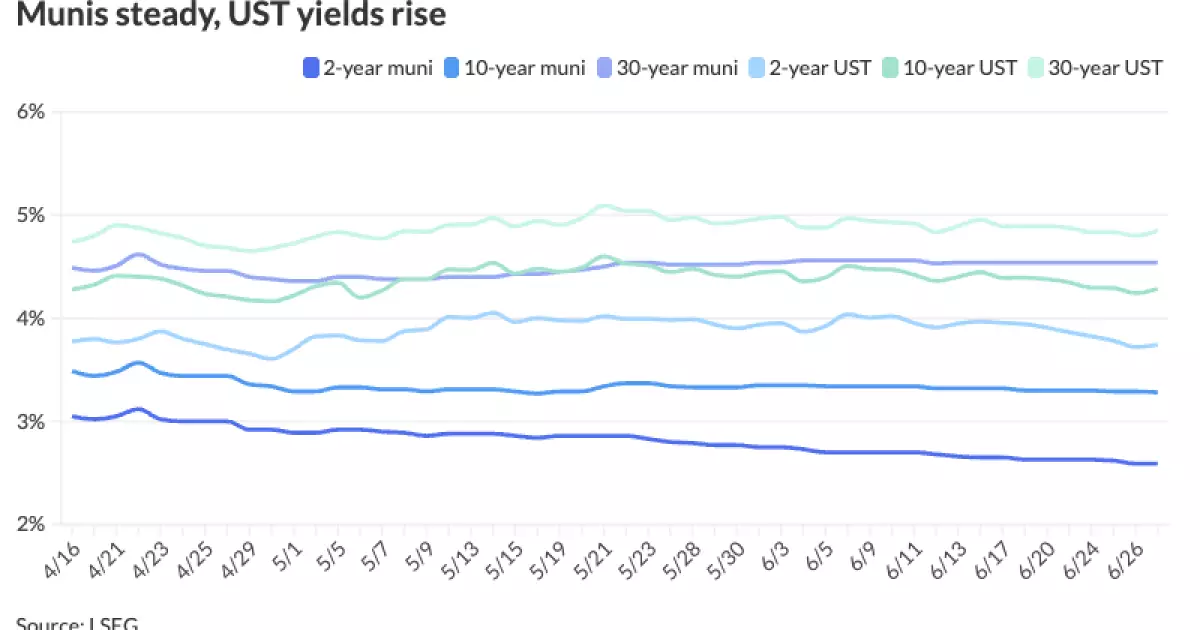

Rising Yields Reflect Shifting Risk Perceptions

Recent data show Treasury yields climbing strongly, with the two-year UST returning 3.745% and the 30-year near 4.85%. Municipal yields and AAA scales have been nudged higher by a basis point or two but lag behind this broader trajectory. The ratios between muni yields and Treasury yields — 69% for two-year and 94% for 30-year maturities — illustrate that municipal bonds remain relatively high priced compared to government debt. This elevated ratio is not just a technical curiosity; it implies that investors are demanding greater compensation for municipal risk, undermining the traditional tax-exempt allure of these instruments. This risk pricing could harden further if economic conditions sour or federal fiscal support wanes.

The Role of Federal and State Fiscal Dynamics

Municipal bonds do not trade in a vacuum—they reflect the fiscal health of states and local governments. With rising expenditures on pensions, infrastructure, and social services, these entities are feeling the pinch. The aggressive issuance that is flooding the market today is often tied to funding gaps born of structural budget shortfalls rather than opportunistic expansions. This fuels a cynical view that municipal issuers are borrowing not to invest in growth but to plug holes. Such a scenario injects uncertainty regarding the sustainability of municipal credit quality. Furthermore, the reliance on tax-exempt status as a shield for investors brings political risk. Should there be pressure to alter tax advantages in a bid to raise federal revenues, the very foundation of muni demand could erode.

Investor Behavior and Market Sentiment

Despite these challenges, many investors are clinging to the belief that municipal bonds will rebound in the latter half of 2025. Barclays and BofA both foresee a back-loaded performance with expectations for market technicals to weaken heading into the fall as issuance outpaces redemptions. This calls into question investor discipline, especially among retail holders who view munis as a “safe” fixed income compromise. The underperformance to date—being the only fixed income asset class with negative total returns year-to-date—is a clear signal that complacency is misplaced. There is a danger in relying on historical resilience and cyclical patterns without acknowledging the evolving macroeconomic context and the fiscal realities municipalities face.

Implications for Center-Right Investors

From a center-right liberal perspective that favors fiscal responsibility and prudent market participation, the current municipal landscape is unsettling. The continued expansion of issuance betrays a tendency among local governments to prioritize short-term fixes through debt rather than structural reforms and efficient spending. Investors should be wary of chasing yield in a market distorted by supply excesses and weakened fundamentals. It is not a question of abandoning munis altogether but rather advocating for a more discerning approach. Playing the muni market today demands vigilance, a clear-eyed understanding of credit quality, and hedged expectations on yield spreads and price stability.

Looking Ahead: Navigating the Muni Market Maze

As we move into the second half of the year, investors face a complicated terrain. Supply might moderate but only after saturating the market in a way that leaves lasting scars. Treasury yields are volatile and likely to remain elevated, pressuring muni ratios further. For those with a stake in fiscal conservatism and stable investment returns, the message is clear: it is time to recalibrate expectations, demand greater transparency on municipal projects, and insist on reforms that enhance the creditworthiness of issuers instead of drowning in a flood of debt that merely postpones reckoning. The myth of municipal bond invulnerability needs to be retired before it does more harm than good to portfolios molded by prudent risk management rather than wishful thinking.