Analyzing the Current Landscape of Municipal Bonds: Trends, Opportunities, and Implications

The municipal bond market is undergoing significant shifts, influenced by various economic factors and investor sentiment. As municipal bonds play a crucial role in financing public infrastructure projects, understanding the dynamics at play is essential for investors, policymakers, and municipal authorities alike. Recent data shows that while municipal bonds exhibited little change in secondary trading, a notable shift in attention to the primary market emerged, primarily driven by substantial new issues and impressive inflows into municipal bond mutual funds.

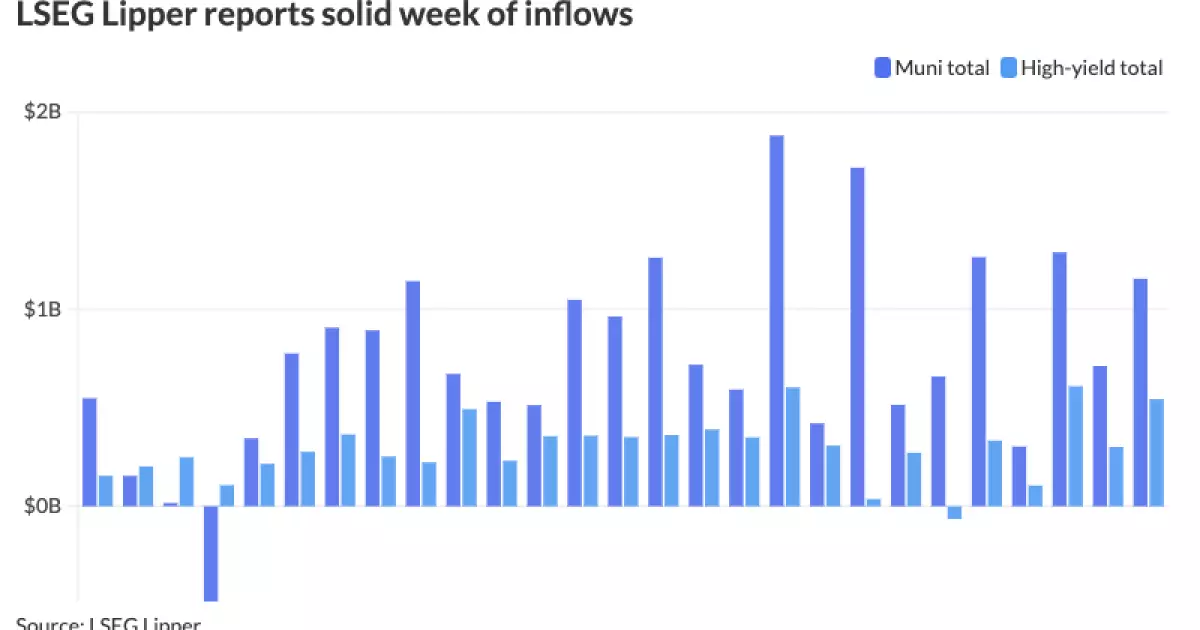

In a remarkable display of investor confidence, municipal bond mutual funds saw inflows surpassing $1 billion as of early December, according to Lipper. This figure reflects a significant increase from the previous week’s revised total of $711.5 million, highlighting an underlying resiliency in the municipal bond market. Notably, high-yield municipal bond funds captured a substantial portion of the inflows, indicating that investors are actively seeking higher returns within this segment. Chris Brigati, a senior vice president at SWBC, emphasized that this pattern suggests that investors are not yet fatigued by market opportunities, retaining an eagerness to buy into municipals.

The ratios of municipal bonds to U.S. Treasuries (UST) offer further insights into market valuation and sentiment. Recent figures indicated these ratios ranging from 61% for the two-year mark to an 82% ratio for the 30-year, as reported by Refinitiv Municipal Market Data. Such statistics illustrate the relative attractiveness of municipal bonds compared to safer UST instruments, which may entice investors seeking favorable opportunities amidst an unpredictable economic landscape.

The primary market remains buzzing with activity, as larger issuers capitalize on favorable conditions. Brigati notes that recent issuances can be attributed to a “simple rebalancing for normal seasonal expectations.” Historically, December has represented a peak issuance month, with historical averages hovering around $31 billion since 2013. However, current projections suggest that a total issuance for December could rise to approximately $500 billion, reflecting heightened urgency among issuers. This is in part a reaction to speculation around potential political shifts—particularly fears surrounding the potential removal of tax exemptions.

The tax exemption for municipal bonds is at the core of the ongoing discourse regarding infrastructure financing. Experts like Matthew Norton and Daryl Clements from AllianceBernstein argue that both major political parties recognize the importance of preserving this exemption to facilitate much-needed infrastructure improvements. The looming threat of its removal not only poses risks to economic growth but could also impede essential local investments. Estimates suggest that eliminating the tax exemption would result in a mere $40 billion savings for the federal budget, a drop in the ocean when juxtaposed with the $6.5 trillion annual budget figure.

A stark consequence of limiting tax exemptions would be to disrupt infrastructure financing, a key area of need across the nation. The prevailing belief among analysts aligns with the notion that the tax exemption will largely be sustained, given its critical role in local economic development.

On the ground, several significant deals reflect a robust primary market. For instance, Barclays recently priced $1.5 billion in transportation bonds for the New Jersey Transportation Trust Fund Authority. J.P. Morgan also initiated a substantial offering of approximately $772.65 million in airport facilities revenue bonds for the Greater Orlando Aviation Authority, showcasing a diversifying set of projects that underline the importance of infrastructure spending.

Moreover, various firms like RBC Capital Markets and Wells Fargo are making sizable contributions through bond offerings, including refunding bonds and revenue bonds across different jurisdictions. These strategic moves not only enhance the liquidity in the municipal bond space but also allow institutions to reallocate capital in a manner that optimally reflects the interests of their investors.

The current state of municipal bonds illustrates a complex interplay of investor confidence, significant political factors, and the necessity for infrastructure financing. As the demand for municipal bonds remains high, observing how issuers adapt to potential changes in regulations will be crucial. The market’s ability to navigate the challenges posed by political constraints, while continuing to attract investor interest, will ultimately dictate its sustained growth and relevance in the broader financial system. The evolution of municipal bonds promises to be a central narrative as we approach the end of the year and beyond, with implications reaching far into the future of public finance and infrastructure development.