The Impending Federal Reserve Rate Cut: Implications and Economic Landscape

As the Federal Reserve approaches an anticipated interest rate cut on December 18, marking its third consecutive reduction, economic observers are closely monitoring how this decision will shape both the short-term and long-term financial environment. Interest rates have already seen a cumulative decline of one percentage point since the Fed initiated its cutting cycle in September, a response aimed at countering the ripple effects of swiftly rising rates that once marked a 40-year inflation peak.

This cautious recalibration underscores the Fed’s deliberative approach amidst uncertainty surrounding economic policies from President-elect Donald Trump during his second term. Jacob Channel, a senior economic analyst at LendingTree, emphasizes that the upcoming rate cut may be the last for a period, hinting at potential pauses in monetary adjustments as the central bank adopts a more wait-and-see methodology. Such strategic caution reflects the need to assess the broader implications of fiscal policy changes in an evolving economic landscape.

The federal funds rate—the interest rate at which financial institutions lend reserves to one another overnight—is crucial in shaping the broader financial landscape. While it does not dictate consumer borrowing rates directly, its fluctuations significantly influence costs that consumers face daily. If the Fed proceeds with the predicted quarter-point cut, the rate will decrease to a range of 4.25% to 4.50%, down from 4.50% to 4.75%.

Economics professor Brett House of Columbia Business School notes that while this adjustment could relieve some financial strain, its effects will not be uniformly felt across all consumer loans. The specific connections between the federal funds rate and various borrowing types reveal a complex interaction that merits careful examination.

One of the most immediate impacts of the Fed’s decisions is observed in credit card interest rates. As many credit cards operate on a variable rate system, they are closely linked to the Fed’s benchmarks. Despite the Fed’s moves to lower rates, average credit card interest rates have surged from 16.34% in March 2022 to an alarming 20.25%. This rise, near historic highs, reflects a trend where credit card issuers are more inclined to raise rates in response to the Federal Reserve than to lower them in anticipation of cuts. According to Greg McBride, chief financial analyst at Bankrate, the response to rate cuts can lag significantly, often taking up to three months.

For consumers grappling with credit card debt, the strategy of switching to a 0% balance transfer card could be more beneficial than waiting for the Fed’s cuts to trickle down. McBride warns that interest rate reductions may not provide adequate relief for those with significant credit card burdens.

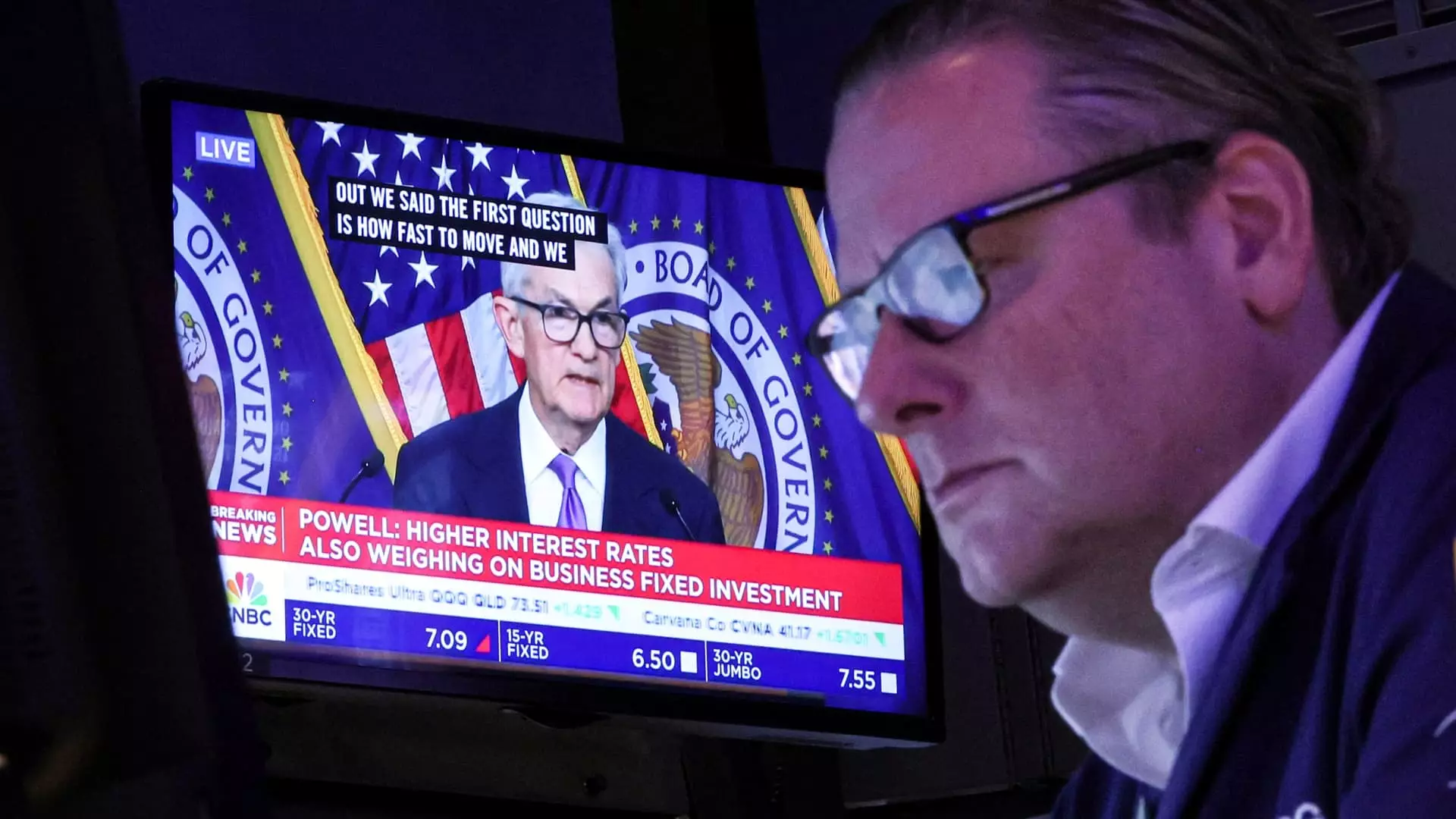

Another key area affected by the Fed’s decisions is the housing market. Fixed mortgage rates, particularly for 15- and 30-year loans, are typically influenced more by economic conditions and Treasury yields than by the Fed’s rate policy. As of early December, the 30-year fixed-rate mortgage stands at approximately 6.67%, a decrease from previous weeks but still significantly above the lows witnessed in late September 2024.

Economist Jacob Channel suggests that future mortgage rate fluctuations will be difficult to predict on a week-to-week basis, underscoring the inherent volatility within the sector. Home buyers looking to secure favorable financing options may need to navigate a complex environment where prices remain high, and financing can strain budgets.

Automobile financing presents another context where the Fed’s actions have indirect effects. Despite fixed-rate auto loans, the rising sticker prices of vehicles compound an already challenging situation, with average financing amounts climbing toward $40,000. Given these high prices, even modest interest rate reductions from the Fed do little to mitigate steep monthly payments, leaving many consumers with budgetary pressures.

Similarly, federal student loan rates remain fixed, insulating many borrowers from immediate impacts from the Fed’s rate cuts. However, those holding private loans with variable rates will likely see reductions corresponding to the Fed’s adjustments. Higher education expert Mark Kantrowitz advises caution regarding refinancing federal loans into private ones due to the loss of essential protections that federal loans provide.

While the Fed’s direct influence on deposit rates is limited, many savings instruments still correlate with the federal funds rate changes. The recent rise in top-yielding online savings account rates, which currently offer nearly 5%, reflects a favorable climate for savers. For the moment, financial experts suggest that this environment could still prove beneficial for conservative investors and consumers.

As the Federal Reserve deliberates on its interest rate policies, the anticipated cuts are poised to impact various sectors of the economy differently. From consumer borrowing to savings, the ramifications of these financial decisions underscore the intricate web of connections that exist in modern economics. As we navigate through this period of adjustment, both consumers and policymakers must remain agile and informed.