Reassessing Municipal Bonds in a Volatile Market: Trends and Implications

As the market gears up to close the year, the landscape for municipal bonds is becoming increasingly complex amid shifting economic conditions. Specifically, the performance of municipal bonds against the backdrop of U.S. Treasury volatility highlights the resilience and challenges facing this asset class. This article delves into key factors affecting municipal bonds, including supply dynamics, interest rates, investor behavior, and market performance metrics.

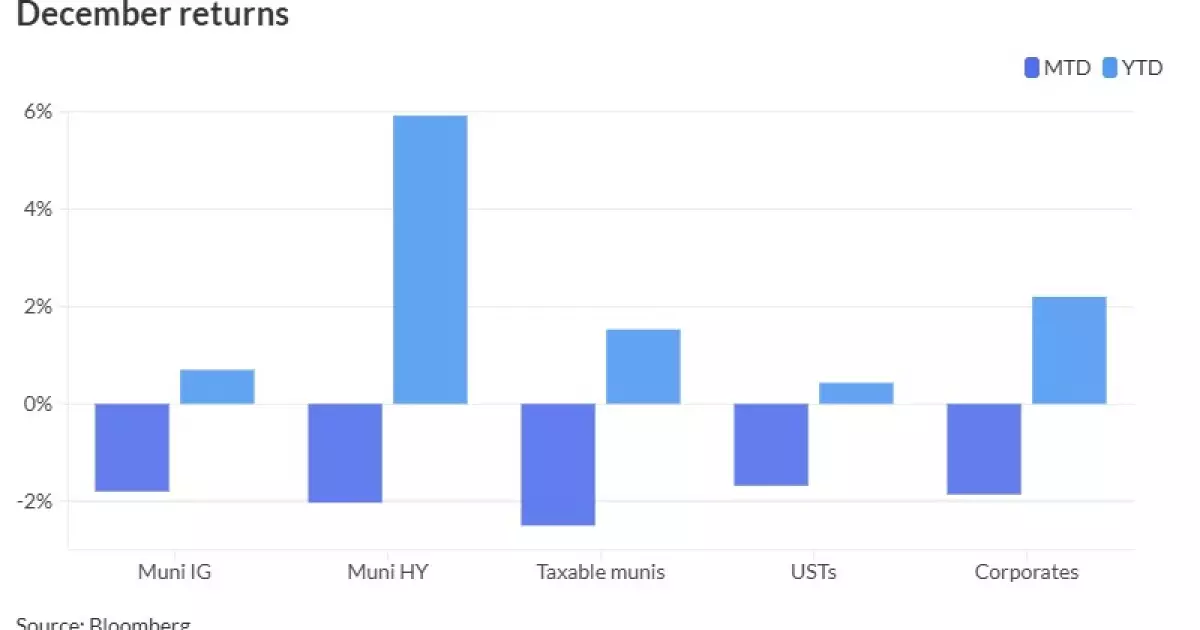

In recent weeks, municipal bonds have shown a notable detachment from U.S. Treasury yields, despite the latter experiencing losses of up to six basis points. The 10-year U.S. Treasury (UST) yield has even ascended above the 4.6% mark. This scenario suggests that while Treasuries are under pressure, investors in municipal bonds are adopting a more measured approach. The Bloomberg Municipal Index indicates a decline of 1.80% for December, a stark contrast to an overall year-to-date return of 0.70%. Such contrasting figures illuminate the asset class’s struggles as the year comes to a close.

Potential causes for this detachment can be traced to market uncertainty and the traditional year-end positioning that often impacts trading volumes. As demand for newly issued bonds wanes—due in part to low new-issue supply—the municipal bond market may find itself at a crossroads, struggling to attract the attention of investors. Market participants are particularly focused on balancing their portfolios before year-end reporting deadlines, which could lead to subdued trading activity.

The upcoming week lacks significant calendar events, with no major new-issue bonds planned, thereby limiting potential catalysts for price movement. The Bond Buyer’s visible supply figure stands at a modest $5.55 billion, hinting at a potential mismatch in supply and demand. Kim Olsan, Senior Fixed Income Portfolio Manager at NewSquare Capital, points out that there exists an $8 billion differential between expected supply and the projected demand stemming from redemptions over the next month. This situation signals that, absent any shifts in supply dynamics, there may be upward pressure on yields if demand continues to soften.

Looking ahead to January, there are forecasts of an uptick in supply with significant issuances expected from various sectors, including Washington State’s competitive offering of $1.05 billion in general obligation bonds. Historically, January is a robust month for municipal bonds; however, the interplay of heightened issuance and Treasury rate fluctuations could create challenges. The cumulative effects of tax reform discussions may also force the hand of issuers, accelerating the timing of municipal supply ahead of fiscal deadlines.

The flow of funds into municipal bonds has remained largely positive this year, a departure from the turbulent financing landscape seen in 2022 and 2023. Investors seem to be navigating a narrower yield range, which has contributed to a more stable environment. Olsan highlights that this year has not experienced a negative loop of rising yields resulting in net asset value (NAV) losses coupled with significant outflows, a trend prominent in the past.

As we approach 2025, early yield perspectives will be critical in determining if investors maintain their interest in the asset class. Historical data shows a tendency for negative fund flows during January, only observed in 2022, which invites speculation on whether this pattern will repeat in the upcoming year.

The relative performance of lower-rated municipal credits has been remarkable, with spreads between A-rated and AAA-rated general obligation (GO) bonds tightening substantially. The ten-year span shows negligible spreads, suggesting that credit quality is becoming paramount in investment decisions. In a year where absolute yields have seen a resurgence to about 4.00%, investors appear receptive to diversifying into lower-rated bonds that offer attractive returns.

Moreover, the contrast in performance between revenue bonds and GOs is widening. Revenue bonds have demonstrated superior returns, outpacing GOs by 60 basis points in 2024. The narrowing of spreads from 2023 to 2024 indicates a shift in investor confidence towards revenue-generating projects, mirroring broader trends within the municipal bond market where credit strength is increasingly under scrutiny.

Looking forward, significant variables will shape the municipal bond landscape, including Treasury rates, supply-demand dynamics, and federal fiscal policies regarding tax reform. The prospect of a possible increase in supply in January, buoyed by an investor-friendly climate, poses questions: Will the strength of demand hold up amid this supply influx? Can the municipal market maintain its positive trajectory into the New Year? As these questions linger, investors will need to remain vigilant in adapting their strategies to navigate the complexities of the evolving municipal bond landscape.