5 Alarming Realities Behind the Current Municipal Bond Market Dynamics

The municipal bond market, often praised for its stability and tax advantages, is currently exhibiting signs of fragility that investors and analysts should not overlook. Despite a seemingly steady start to the week with minor increases in muni yields and firmer Treasury bonds, the overall picture is far from reassuring. Market participants cite limited volatility and negligible price movements — a deceptive calm masking deeper challenges. While yields on short-term municipal bonds edged down marginally, the long-term maturities stubbornly held ground, indicating that the market is grappling with uncertainty rather than resilience.

This stagnant behavior is symptomatic of a market stuck in limbo, where investors recognize value but struggle to find compelling catalysts to drive outperformance. The technicals, underpinned by small but steady fund inflows, are insufficient to ignite meaningful momentum. Indeed, the ninth consecutive week of positive inflows into municipal mutual funds — a modest $76.9 million last week — pales in comparison to the scale of liquidity needed to significantly rally the market. The lack of enthusiasm speaks to a wider hesitation in the face of looming fiscal constraints and economic headwinds.

Why Ratios and Spreads Signal a Troubling Tilt Toward Risk

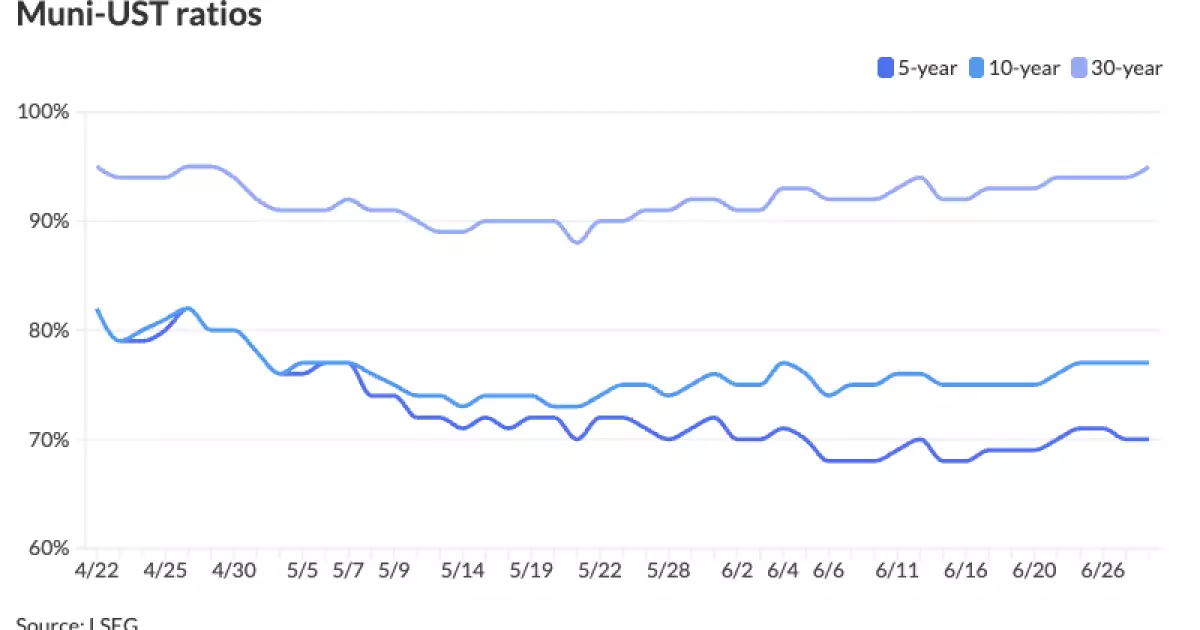

A critical indicator in municipal finance is the basis-point spread between muni yields and U.S. Treasury yields, often expressed in ratios. Recent data shows these ratios drifting wider, especially in long maturities—from about 77% at the ten-year mark to 95% at 30 years according to various data providers. While at first glance wider spreads might trumpet opportunity, they more accurately reflect an underlying risk aversion as investors demand greater compensation for lending long term to municipalities amid fiscal uncertainty.

This dynamic is troubling from a center-right, fiscally prudent perspective. Municipalities have historically been considered safe bets due to their ability to tax and budget for bond repayment. However, increasingly generous spreads suggest that investors view these bonds as less secure or expect future financial stress—possibly triggered by pension liabilities, inflationary pressures, or unsustainable debt—thus warranting a risk premium. This skepticism should serve as a signal for policymakers to address structural budget gaps and improve transparency if they are to restore investor confidence.

July’s Cash Flows: A Double-Edged Sword

The inflow of principal repayments and interest payments scheduled for July presents both relief and risk. Investors will receive upwards of $54 billion in combined principal and interest, with heavy redemptions weighted in fiscally strained states such as California, New York, and Florida. At face value, this seemingly abundant liquidity might be viewed as a boon, providing a buffer and encouraging bond issuance.

Yet, this influx also pressures the market to absorb upcoming supply, which, although muted this week due to the July 4th holiday, will ramp up significantly mid-month. Important deals on the horizon include sizable issuances from New York State and the California Community Choice Financing Authority, some topping $1 billion. While the market has historically managed to digest such volumes, increasing debt issuance amid uncertain economic fundamentals raises concerns about long-term market sustainability. The influx of “generous after-tax yields,” especially in high-grade deals pricing above 8% tax-equivalent yields, may reflect a market pricing in elevated credit risk rather than purely attractive returns.

Is the Federal Government’s Role in Muni Markets Overestimated?

There is a lingering overreliance on the Federal Reserve’s influence permeating fixed income markets, including municipals. While the Fed’s signaling on interest rates affects Treasury yields, municipals are subject to a more complex set of factors that the central bank cannot fully control. The relative strength or weakness of municipal bonds depends largely on state and local fiscal health, which has been stressed by the pandemic’s aftermath and inflation-induced budget pressures.

From a center-right lens, this is a telling reminder that prudent fiscal governance at the state and local levels cannot be outsourced to federal policy. The lack of a clear catalyst for municipal outperformance signifies not only market caution but also an implicit call for municipalities to enact responsible spending reforms. Without such measures, investors might continue demanding wider spreads as insurance premiums against potential defaults or downgrades. The Fed’s role, while important in shaping broader interest rate environments, is secondary to fundamentals in this space.

The Illusion of Stability: Why Investors Must Be Cautious

Municipal bonds have long been a cornerstone of conservative investment portfolios, thanks to their tax advantages and perceived safety. However, the recent data reveals subtle fractures in that perception. The modest rally since mid-April, which has recouped some losses after a steep dip, still leaves year-to-date returns barely in the black, highlighting that the muni market is far from a reliable safe haven in the current environment.

Moreover, despite primary market activity attracting strong demand due to attractive spreads, the overall health of municipal finance remains uncertain. Heavy redemptions concentrated in states with large pension burdens and rising social service costs could presage credit events that might roil the market. Investors complacent about muni risk would be wise to reassess underlying credit quality rather than chase yields blindly.

In this light, municipal bonds feel more like an overweighted component in portfolios than a bulletproof fortress. The run-up in yields might indeed seem exciting, but it carries a clear warning: higher compensation for risk does not equate to risk-free profits. Only municipalities that implement genuine fiscal discipline and show transparent budget management can hope to restore true investor confidence — and until then, patience and selectivity should dominate investment decisions.