Why the Municipal Market Crisis Is a Wake-Up Call for Conservative Investors: 5 Shocking Truths

The recent stagnation and underperformance of municipal bonds, especially compared to other asset classes, should serve as a loud wake-up call for center-right investors who believe in cautious, disciplined investment strategies. Despite the typical reputation of munis as stable, tax-advantaged havens, the first half of the year has exposed alarming vulnerabilities. Municipal bonds are outright losing value—long-term instruments in particular—highlighting structural issues that threaten their longstanding appeal.

This anomaly signals that simplistic faith in munis as foolproof income vehicles no longer holds water. It’s evident that factors like supply-demand imbalances, rising costs, and shifting investor preferences are drastically reshaping the landscape. For conservative investors, this is more than a blip; it’s a stark reminder that markets are complex systems riddled with hidden risks, and complacency can be costly.

Market Myths and the Reality of a Troubled Muni Landscape

The optimistic narrative surrounding munis as a “safe” investment instrument is increasingly challenged by the data. Year-to-date, tax-exempt municipal bonds have lost roughly 4% in value—the worst among fixed-income categories—while corporates and Treasuries have gained. This divergence signals a serious misalignment.

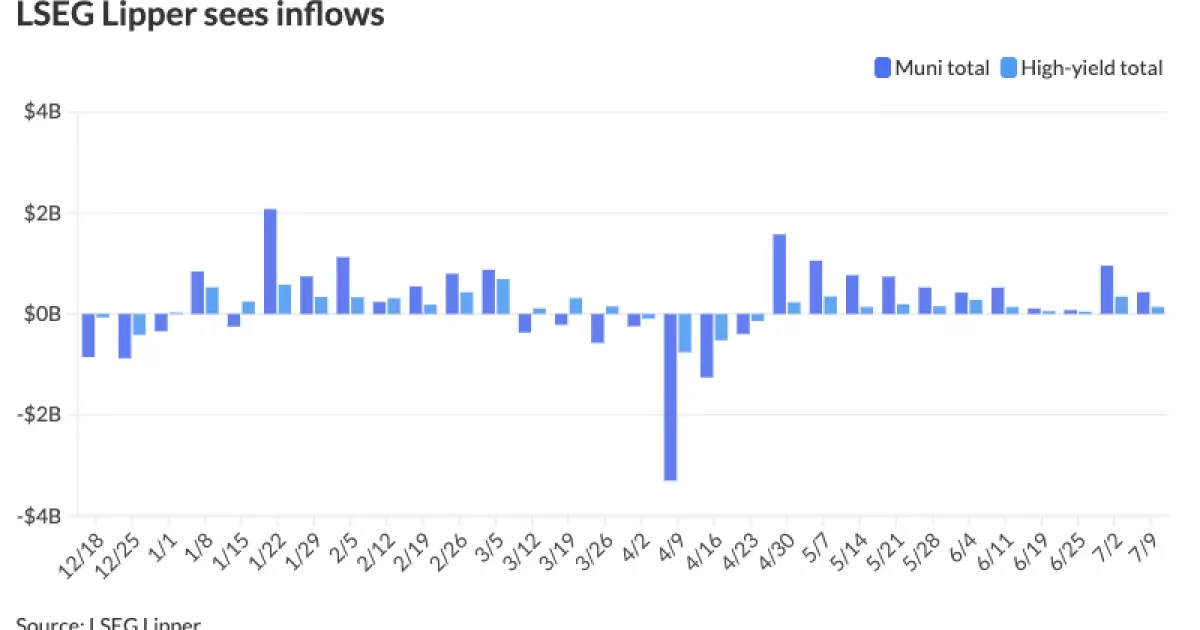

Much of this distress stems from a combination of supply pressure and structural shifts. As the first half of the year saw an issuance boom of approximately $280 billion, driven by fears over the potential loss of tax exemptions, the market became choked with supply. Ironically, the recent legislative victory—”One Big Beautiful Bill”—preserved the tax advantage, but the damage to investor confidence had already been done. Investors, spooked by the large influx of new issuance and inflation’s rising costs, have begun to retreat, raising yields and pushing prices lower.

This forced a steepening of the muni yield curve—indicative of a market under stress—and a realization that the supposed safety of municipal bonds is more fragile than the many industry proponents claimed for years. The long-end of the curve, often considered a safe haven, is especially vulnerable, demonstrating that even the most conservative muni investors may need to rethink their assumptions.

The Fundamental Risks: Supply, Inflation, and Changing Investor Flows

The prevailing issue isn’t just market sentiment; it’s systemic. Supply-side factors remain acutely problematic. Issuance was aggressive, motivated by fears of losing tax advantages, and now the market faces a potential slowdown in new supply due to legislative clarity. But that doesn’t reverse the damage already done. The backlog of projects and increased project costs—fueled by inflation and dried-up pandemic aid—compound the problem.

Meanwhile, investor flows are transforming. Increasingly, funds are avoiding the long end of the muni curve, favoring shorter-term assets or alternative instruments like ETFs and separately managed accounts. The shift indicates a regional and structural change in investor preferences, uncomfortable for many traditionalists who relied on munis for stability and predictable income.

This behavioral change is pivotal. It signals that the perceived safety net of munis as a long-term hold is weakening. The idea that munis are the “conservative safe haven” must be reconsidered. They are vulnerable to macroeconomic shifts, fiscal policy uncertainties, and investor sentiment—factors that can turn a seemingly stable market into a perilous one almost overnight.

The Political and Fiscal Implications: Who Pays the Price?

In a broader political sense, the muni market’s struggles reflect ongoing tensions in fiscal policy, government spending, and public infrastructure funding. The fact that the recent legislation preserved tax exemptions suggests political resolve to protect municipal bonds, but it also complicates fiscal management. Governments and issuers face increasing costs driven by inflation, yet bondholders face declining yields and capricious markets.

Center-right investors, who often advocate for fiscal discipline and limited government intervention, should scrutinize this scenario closely. The market signals that unchecked issuance, coupled with rising costs and investor caution, can distort fundamental valuation. There’s an implicit warning here: reliance on the facade of municipal stability might be misguided, especially when fiscal prudence is compromised by political pressures.

The potential for a downturn—if the Federal Reserve cuts rates and liquidity floods back into munis—also raises questions about timing and resilience. Even if a temporary rally ensues, underlying issues remain unresolved. Defensive positioning demands seeing through the short-term noise and understanding that munis are increasingly subject to macroeconomic shocks.

For investors aligned with a conservative, center-right philosophy, the current muni market is a stark lesson. It underscores that no asset class is immune to macroeconomic vulnerabilities. The long-standing assumption that munis are an invincible component of a balanced portfolio needs realigning with reality.

Market conditions are shifting, and the conventional wisdom about munis’ safety is being challenged by hard data and structural trends. It’s no longer enough to cling to historical comfort zones. Instead, a nuanced approach—focused on active management, diversification, and understanding inherent fiscal risks—is essential. The muni market’s stumble might be temporary, or it might mark the start of a more enduring correction. Either way, this crisis underscores the importance of skepticism, vigilance, and strategic evolution in conservative investing.