The Evolving Landscape of Municipal Bonds: Trends and Insights

The municipal bond market has presented a complex picture as it approaches the fourth quarter of the year. Despite facing declining yields for four consecutive sessions, this sector remains resilient amid fluctuating broader financial conditions. On Wednesday, municipal yields saw reductions of up to three basis points, mirroring losses in the U.S. Treasury while equities in the market made noticeable gains. Fresh developments have pushed the two-year U.S. Treasury yield past the significant 4% mark, a level not seen since August, prompting investors to reassess their strategies.

The differential between municipal bonds and U.S. Treasuries remained notable, with the two-year muni-to-Treasury ratio resting at 61%, indicating that investors are still seeking the relative safety offered by municipal yields. Agencies like Refinitiv and ICE Data Services continue to provide valuable insights into market trends and yield comparisons, revealing a consistent demand for munis even as broader yield curves adjusted.

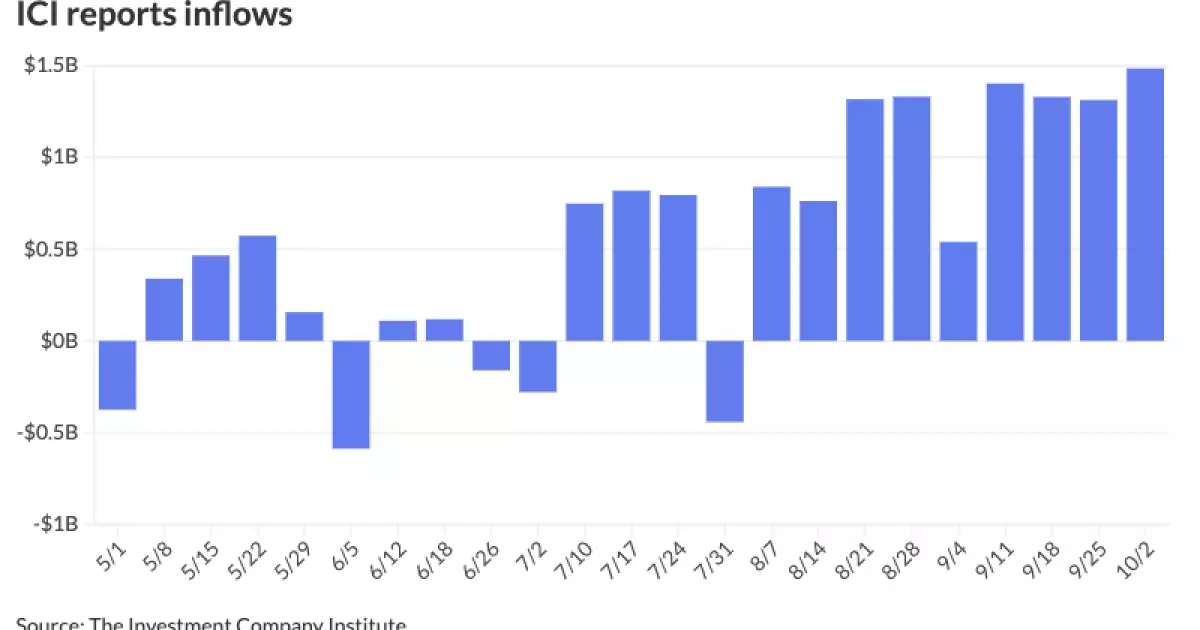

Remarkably, the Investment Company Institute has reported robust inflows into municipal bond mutual funds, totaling $1.484 billion for the week ending October 2, following $1.312 billion the previous week. This marks an impressive nine weeks in a row of inflows exceeding the billion-dollar threshold. Moreover, exchange-traded funds (ETFs) in the municipal sector recorded a substantial influx of $810 million—an increase from the preceding week’s $109 million.

Experts, such as Jeff Lipton, have pointed out that while the market reflects active trading, particularly with large municipal issuers front-loading their bonds ahead of the presidential election, there are underlying forces shaping market stability. The technical landscape indicates a potential for clients to seize opportunities as supply and demand in the market continually adjusts to various external pressures.

In analyzing the current state of the municipal bond market, it is crucial to consider the economic indicators that influence investor behavior. Recent data suggest a gradual shift in the Federal Reserve’s approach toward rate adjustments, resulting in a more cautious outlook. A sell-off in the UST market at the start of the week caused some apprehension, yet strong reinvestment needs in October have buoyed demand for munis.

Daryl Clements, a municipal portfolio manager at AllianceBernstein, suggests that while pricing appears relatively high, continued macroeconomic stability allows for profitable buying opportunities. This chapter in the bond market seems motivated by a combination of tactical asset allocation decisions aimed at maximizing returns, particularly as the Federal Open Market Committee meets and makes decisions affecting overall market liquidity.

As prospective investors digest market movements, varying levels of sentiment across retail and institutional buyers are becoming apparent. While institutional investors may gravitate towards relative value assessments, retail participants are encouraged to consider taxable equivalent yields. Such calculations can clarify the potential benefits of municipal investment versus alternatives, especially in periods characterized by fluctuating yields.

In a notable market move, Siebert Williams Shank priced a substantial $935 million of general obligation (GO) bonds for Connecticut, reflecting ongoing confidence in the municipal bond market and its appeal to investors. Specific tranches featured competitive yields, indicating that while overall pricing might feel tight, there remains substantial appetite for high-quality issuances.

As we move closer to the conclusion of 2023, the municipal bond market is poised for continued adaptation. Market analysts predict a potential softening in supply ahead of the presidential election, which could resurface towards the end of the year. By this time, the reinvestment needs and evolving economic conditions could create new opportunities for discerning investors.

Looking forward, the blend of strong institutional and retail interest, coupled with robust supply dynamic, positions municipal bonds as a compelling space to watch. While the fourth quarter traditionally introduces complexities—given seasonal market adjustments—experienced stakeholders recognize the opportunities inherent in recognizing the cyclical nature of these bonds. The foundation laid during this pivotal year appears to support sustainable growth as we transition into 2024, inviting investors to navigate potential shifts with informed strategies.

The municipal bond landscape remains vibrant and multifaceted, showcasing not only the adaptability of market actors but also the continuous interplay of economic factors that will shape future performance. As we look ahead, prudent evaluation of both risks and opportunities will guide investment decisions, fostering a nurturing environment for enduring aspirations in the municipal segment.