Record-Breaking Bond Issuance: An Analysis of 2024 Trends

The bond issuance landscape in 2024 has witnessed a remarkable surge, signaling a potential breakout year for municipal bonds. As of September, data reflects that this surge is not only considerable but also consistent, marking nine consecutive months of year-over-year increases and establishing a new rhythm in the market that could redefine municipal financing.

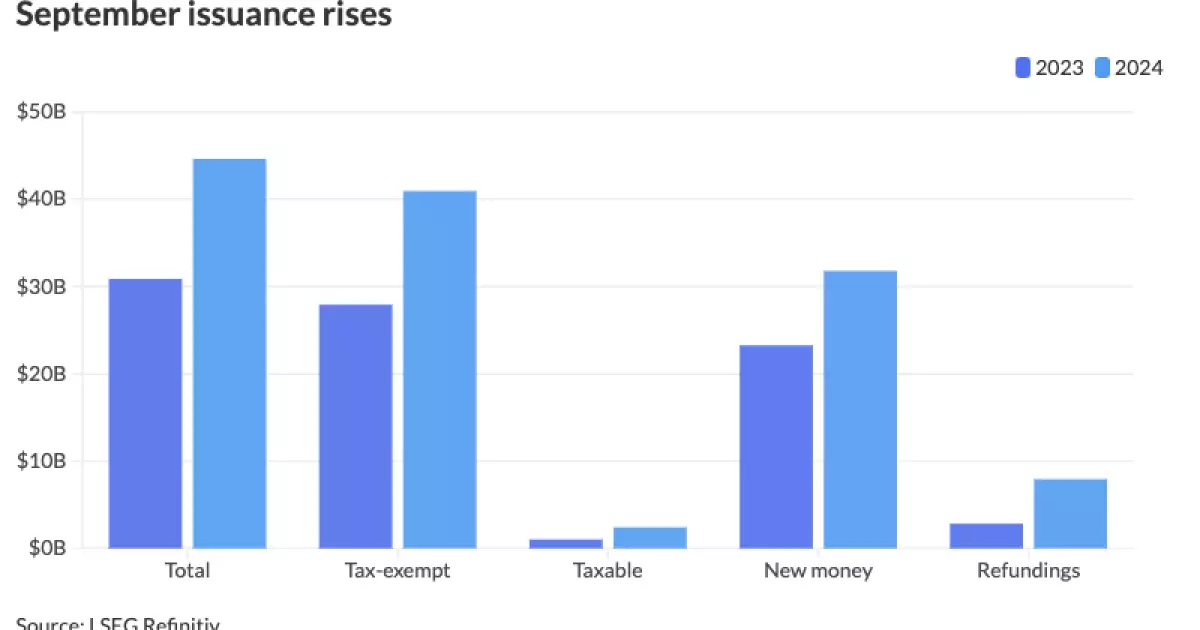

September 2024 proved to be a monumental month for bond issuance, with a staggering total of $44.628 billion spread across 752 issues. This figure represents a robust 44.5% increase from the comparable month in 2023, which saw only $30.88 billion across 619 issues. Such a leap in issuance highlights a market that is regaining its footing as issuers look to capitalize on favorable financing conditions while preparing for impending election-related uncertainties. This year’s September numbers not only surpass the previous year’s but also exceed the 10-year average of $35.679 billion, revealing a newfound confidence among issuers.

Year-to-date issuance stands at approximately $380.423 billion, reflecting a 35.2% increase compared to last year. At this rate, it is poised to eclipse the total from 2023, which was $384.715 billion. However, to achieve a new record surpassing 2020’s high at $484.601 billion, issuers will have to deliver more than $104 billion in the final quarter of the year—a significant challenge in a typically volatile period.

The increase in issuance can be attributed to multiple factors. A primary driver appears to be the winding down of pandemic-related financial support, which has pushed state and local governments to address new funding needs. As the COVID-19 aid package fades into history, there is a pressing necessity for municipalities to engage with the bond market for fresh capital. This scenario has prompted issuers to act promptly, seeking to lock in favorable rates before uncertainty spikes ahead of the presidential elections.

Moreover, taxation trends are also illuminating the landscape. Tax-exempt issuance in September increased significantly to $40.944 billion, up 46.6% from the previous September, while taxable issuance surged by a staggering 135.6% to $2.422 billion. The appetite for new-money deals rose by 36.7%, further illustrating a general eagerness to leverage the current financial environment while capital is readily available.

The market’s preference for larger deals has become increasingly apparent. Year-to-date statistics suggest that the occurrence of “mega deals”—those exceeding a billion dollars—is becoming the norm rather than the exception. Notable transactions, such as the $1.6 billion general obligation bonds from Washington, D.C., and the equally significant Texas Water Development Board’s revenue bond issuance, encapsulate this growing trend.

Investment managers note the heightened investor demand for these hefty offerings, indicating a robust liquidity environment and a willingness among issuers to pursue larger debt financing. This acceptance not only enhances competition among issuers but also facilitates a healthier, more dynamic market.

Looking ahead, the cyclical nature of municipal bond issuance in conjunction with the timing of elections suggests that activity will continue to rise in the weeks leading up to November. Historically, bond issuance spikes before major elections due to strategic planning by municipalities aiming to escape potential market volatility. However, analysts caution that a short-term dip in activity may occur immediately before the elections, followed by a rebound toward the end of the year as issuers endeavor to generate financing against impending borrowing needs.

The previous two election cycles, specifically in 2016 and 2020, showed significant issuance volumes during the fourth quarter, suggesting similar patterns could emerge in the upcoming months. Anticipating this, officials and strategists alike are bracing for a wave of transactions as 2024 unfolds.

The data reveals striking performance disparities among states, with Texas leading the way year-to-date with $56.138 billion in bond issuance, marking a 12.5% increase over last year. California and New York follow closely, reflecting the substantial economic activities and financing needs of these populous states. Florida’s remarkable 117.8% increase further underscores the varied financial landscapes across the nation.

Overall, the robust recovery and resilient issuance patterns signify an evolving bond market geared for growth. This strategic market positioning allows local governments to more effectively address pressing financial needs, presenting a pivotal moment for both issuers and investors moving forward.