The Shifting Dynamics in the Municipal Bond Market: An Analytical Overview

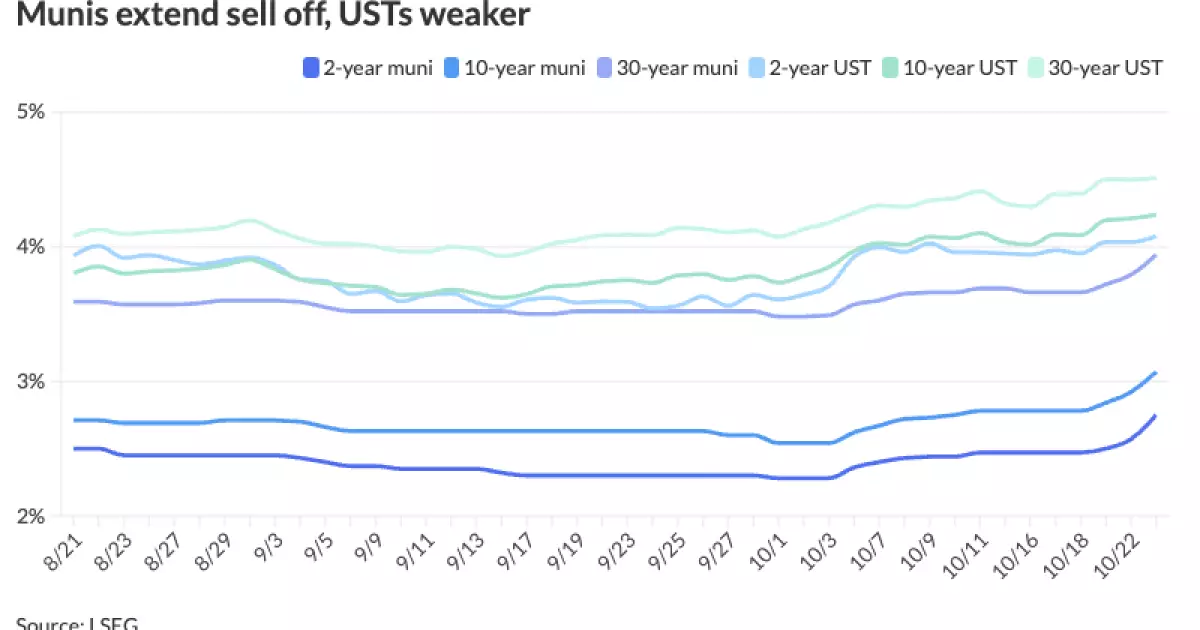

The municipal bond market has recently experienced significant volatility, marked by a pronounced correction on Wednesday. This shift can be traced back to a broader alignment with the U.S. Treasury yields, which have seen a steady increase over the past few weeks. This disparity in performance had led municipal bonds to appear overvalued, making a corrective pullback almost inevitable. Yields within the municipal sector surged anywhere from five to 18 basis points, breaking the 3% threshold on a 10-year yield for the first time since early July. Meanwhile, U.S. Treasury yields experienced a milder increase, reflecting a somewhat weaker dynamic in comparison.

This correction highlights the interconnected nature of different fixed-income markets. As yields rise in one sector, others often follow suit, especially when prior valuations seem excessive. The data shows ratios rising for municipal bonds compared to Treasuries, stressing the necessity for a reevaluation of pricing dynamics.

Market experts like Kim Olsan from NewSquare Capital suggest that this correction was overdue, given the “one-way trade up in yield” observed in U.S. Treasuries previously. The disparity in movement indicates a lag in the municipal market’s response to the overall economic landscape. Significant factors such as increasing bid-wanted counts, burgeoning dealer inventory, and rising money market balances reflect a cautious sentiment prevailing among investors.

The correlation between rising Treasury yields and municipal rates cannot be understated. With Treasury rates up sharply due to political uncertainties surrounding imminent elections—particularly in light of a potentially favorable outcome for Republican candidates—concerns over deficit spending and inflation remain at the forefront. Such apprehensions naturally ripple through all fixed-income sectors, including municipalities, thereby affecting liquidity and investor confidence.

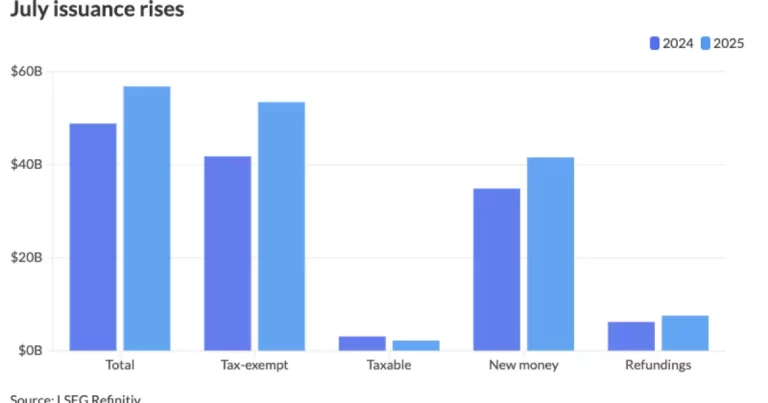

Amidst this evolving backdrop, there’s a palpable acceleration in municipal supply. This is primarily driven by issuers eager to secure necessary funding before potential shifts in policy following the elections. The urgency has led to changes in the pricing of municipal debt, a move that financial strategists like James Pruskowski from 16Rock Asset Management interpret as an effort to recalibrate market dynamics.

The influx of new capital is observed alongside a decline in reinvestment opportunities, which are at near-annual lows. The implications are clear: as new issuances come to market with attractive yield levels, investors have begun to pivot, thereby presenting a potential bottoming opportunity in the muni sector.

Despite the tumultuous environment, there remains a strong undercurrent of investor interest in municipal bonds. Recent data from the Investment Company Institute showcases steady inflows into municipal bond mutual funds, totaling $1.524 billion for the week ending October 16, marking an 11-week streak of positive inflows. Additionally, the behavior of exchange-traded funds also reveals a resurgence, as they recorded $1.205 billion in inflows against previous outflows.

This sustained inflow signals a robust basal demand for municipal bonds despite erratic yields. As more holders navigate the muddied waters of the bond market, the underlying fundamentals may continue to promote investment despite alarming yield spikes.

The primary market witnessed several noteworthy issuances, indicative of the strategic adjustments higher yields demand. For instance, the New York City Transitional Finance Authority issued a substantial $1.5 billion in bonds, which saw significant yield increments from prior pricing. Moreover, the Ohio Housing Finance Agency and the Regents of the University of Colorado had similar experiences, with increased yields mirroring market corrections.

These actions take on a dual significance: not only do they reflect a necessary alignment with prevailing market conditions but they also exhibit the resilience and adaptability of issuers in responding to legislative and economic influences. The upcoming bond issuances from various authorities, including the California Community Choice Financing Authority and the Virginia Small Business Financing Authority, continue the trend of responding to market expectations.

As municipal bond markets weather the current corrections, the focus must shift toward understanding the underlying sentiments driving these changes. The intricate balance between supply, demand, and external macroeconomic pressures will undoubtedly shape the trajectory of municipal bonds in the coming weeks. Investors are advised to remain vigilant, as the landscape continues to evolve amidst fluctuating yields and political uncertainty, ultimately defining the future health of the municipal bond market.