Market Overview: Analyzing October’s Muni and Treasury Performance

The end of October has brought a notable shift in the municipal bond (muni) market alongside fluctuations in Treasury yields, marking a particularly significant month for investors. As we conclude the final session, the dynamics of the market’s response to yield adjustments and investor flows bear closer examination.

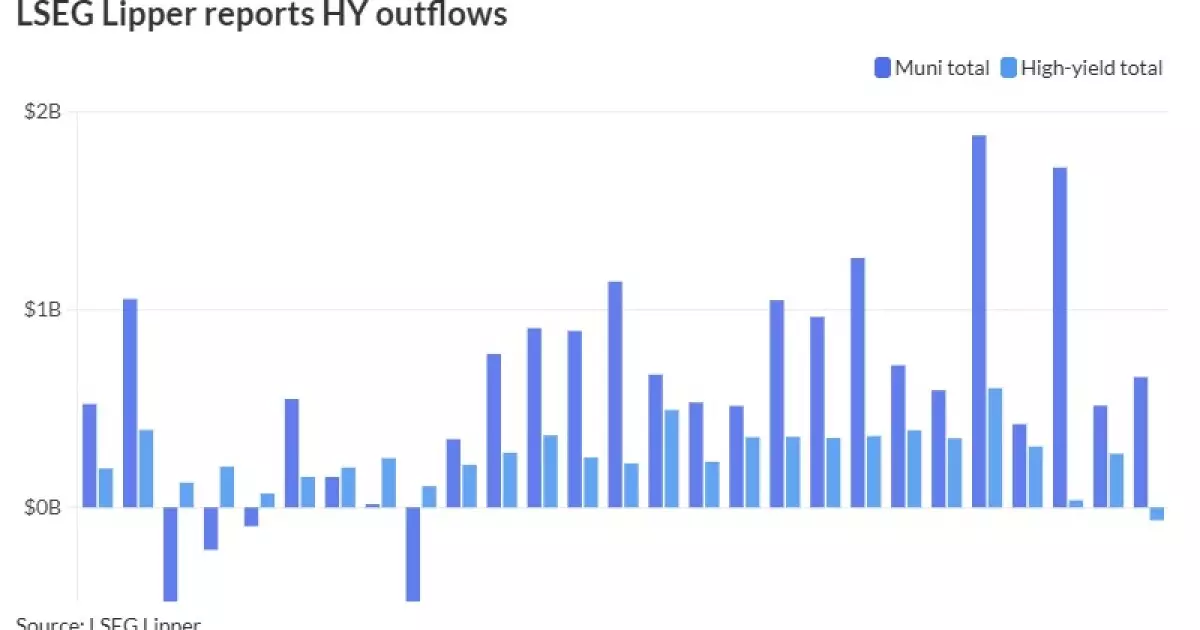

In the closing days of October, munis have demonstrated a relative stability in pricing with minimal movement. Notably, the municipal mutual funds have enjoyed significant inflows; however, high-yield segments have experienced their first outflows since mid-April, indicating underlying caution among investors. With the recent performances of U.S. Treasuries showcasing mixed results and equities sustaining losses, the behavior of municipal bonds becomes particularly interesting. Kim Olsan, a senior fixed income portfolio manager at NewSquare Capital, captured the sentiment aptly, noting an attractive yield curve that has emerged alongside corrections in the market. Despite the backdrop of corrections leading to real losses—the Bloomberg Municipal Index, for instance, experienced a decline of -1.51%—Olsan emphasizes that this correction, while worrying, should be contextualized within historical trends. Indeed, this represents the largest loss since October 2009, overshadowed by the more substantial decline in U.S. Treasuries, which sit at -2.42%.

The month of October has ushered in broader spreads and heightened yields, which now capture the interest of a wider investor base. Olsan flagged that the short end of the municipal yield curve presents opportunities that warrant a defensive approach, particularly as fixed one-year maturities on single-A revenue bonds are currently yielding around 3.20%. The adjustments noted by Olsan highlight a shift whereby higher taxable equivalent yields (TEY) now hover in the mid-5% range, significantly outpacing U.S. Treasuries by over a percentage point—a persuasive factor for cautious investors.

The discussion then advances to the intermediate range, where AAA-rated 10-year bonds have breached the 3.00% threshold. The implications are profound as they signal a critical juncture for stakeholders, especially as allocations toward higher-rated bonds potentially signify a pursuit of stability in an otherwise volatile landscape. As Olsan pointed out, Washington State’s recent GO bond draws attention with a yield of 3.24%, translating into a TEY of 5.40%—demonstrating the continuing demand for robust municipal offerings.

Amid the market’s shifting landscape, transactions also provide crucial insights into investor sentiment and behavior. The issuance of substantial bond packages continues, illustrated by BofA Securities’ pricing of $188.895 million in sustainability lease revenue bonds for Washington state. With various maturities yielding between 2.97% and 4.30%, these bonds reflect the diverse appetite for municipal debt among investors, particularly in sustainable financing avenues. Additionally, other competitive markets remain active, like the Charleston County School District’s sale of general obligation bonds, which further demonstrate robust municipal activity despite fluctuations in the broader market.

Interestingly, while October recorded the highest monthly supply of over $56 billion, forward issuance is set to take a dramatic decline into November. The visible supply noted by the Bond Buyer shows a stark drop to $3.77 billion, hinting at a potential lull in new bond offerings as the market adjusts and strategizes around the upcoming elections.

On the inflow front, data from LSEG Lipper reveals a continued positive trend with a noteworthy addition of $659 million into municipal bond mutual funds. This marks an impressive streak of 19 consecutive weeks of inflows, underscoring persistent investor confidence in the segment. However, the outflow of $64.4 million from high-yield funds signals a precautionary shift among investors who may be reassessing risk in light of recent volatility. Notably, long-term funds captured the majority with $361 million, while interest in intermediate-term funds solidified their standing as preferred vehicles for cash allocation.

Amidst this, the juxtaposition of inflows into municipal exchange-traded funds against the substantial inflows to cash management, with money market funds experiencing $2.518 billion of inflows, speaks volumes about investor strategies under uncertainty. The declining yields in money-market funds alongside the SIFMA Swap Index call for careful watch as market dynamics continue to unfold.

In summation, as we close the chapter on October, the trajectory to year-end presents both challenges in terms of market corrections and budding opportunities characterized by favorable yield curves in the municipal space. Investors must navigate these fluctuations with acute awareness while capitalizing on the emerging trends and insights that are redefining the current landscape of fixed-income investing.