Current Trends in the Municipal Bond Market: An In-Depth Analysis

As the municipal bond market continues to stabilize, distinct patterns are emerging that reflect broader economic conditions alongside seasonal influences. Recently, municipals demonstrated a steady performance, and several noteworthy developments in the primary market have been particularly illuminating. This article examines the current state of municipal bonds, focusing on yield fluctuations, inflows, and issuer behaviors in light of impending economic uncertainties.

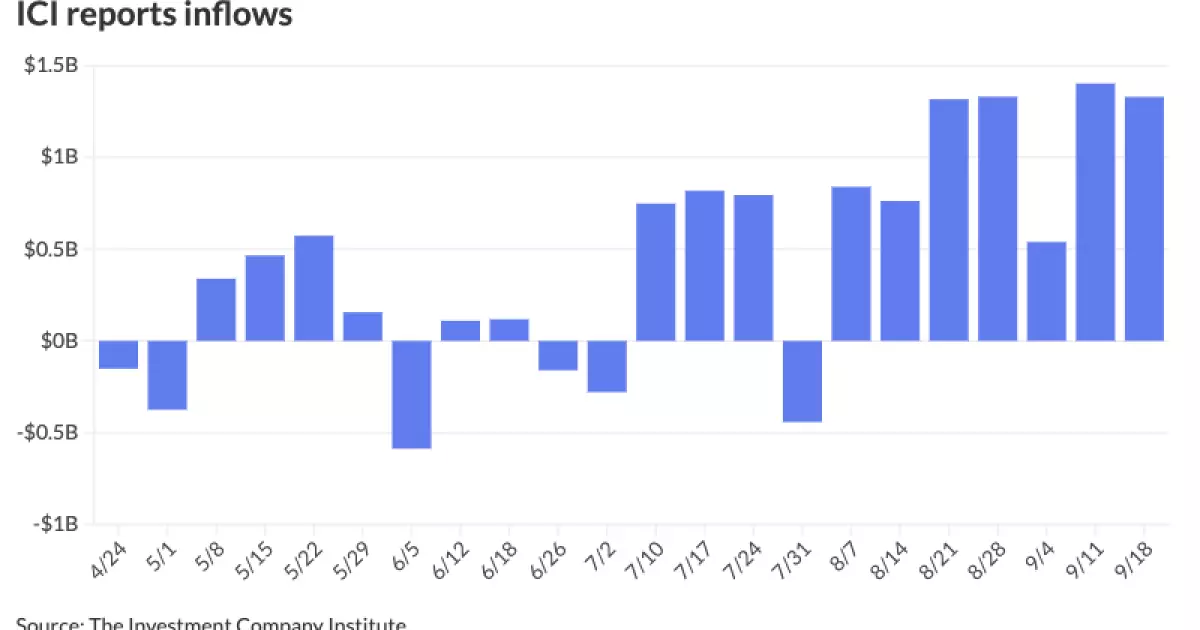

The municipal bond market has shown resilience, with yields showing a downward trend as large transactions were repriced. U.S. Treasuries exhibited weakness, and equities faced challenges as well. According to the Investment Company Institute, the week ending September 18 witnessed $1.329 billion in inflows into municipal bond mutual funds, although this figure was slightly lower than the $1.402 billion reported the previous week. Notably, exchange-traded funds (ETFs) experienced inflows of $55 million, which is another significant decrease compared to the previous week’s $1.048 billion.

Market analysts at Appleton Partners emphasize a pivotal transition as the summer season concludes, highlighting the departure of substantial reinvestment capital that has characterized the market during this period. They foresee increased volatility as seasonal issuance processes accelerate in the coming weeks due to a mix of heightened supply and diminished reinvestment. This shift presents both challenges and opportunities for investors as they navigate a landscape poised for potential fluctuations.

Issuance levels have recently surged, with recent weeks showing nearly $14 billion in supply, illustrating strong market activity. A notable part of this increase can be attributed to issuer caution in anticipation of market volatility tied to the upcoming presidential elections. As highlighted by Jon Mondillo, global head of Fixed Income at abrdn, many issuers are incentivized to act before November 5, 2024, due to uncertainties that may follow the elections. This proactive approach indicates a strategic response to potential fiscal instability depending on electoral outcomes.

Appleton Partners’ strategists argue that the combination of increased issuance and restricted reinvestment demand could temporarily lift yields, potentially presenting attractive prospects for municipal investors. They also point out that current muni-to-UST ratios, notably around 70% for ten-year bonds, could further elevate if supply remains outsized, adding value to municipal investments. Notably, the long-term ratios remain a point of focus, having historically hovered near 85%–86% compared to the previous trends where they were significantly higher.

The primary market has recently seen substantial activity. On a record-setting Tuesday, two billion-dollar municipal deals emerged, particularly for New York. This trend continued into Wednesday as new issues were priced, showcasing decreasing yields for several issuances. Among these, Bank of America Securities priced a significant $1.061 billion of consolidated bonds from the Port Authority of New York and New Jersey, indicating substantial demand in institutional markets.

The bond pricing reflected a strategic repricing across various maturities, reinforcing the anticipation of future market conditions. Additionally, BofA Securities also handled the pricing of electric system revenue bonds for the Salt River Project, which experienced yield adjustments but still demonstrated robust investor interest. Various entities, including Texas school districts and airport districts, also engaged actively, highlighting sustained demand even amidst fluctuating economic signals.

As municipals continue to adapt to evolving conditions, market participants are anticipated to closely monitor the interplay between issuance levels, yield ratios, and broader economic indicators. The current landscape suggests that municipal bonds will remain attractive given the relative stability they offer compared to Treasuries, particularly as yield ratios appear rich, especially on the long end.

Investors should be prepared for more pronounced volatility as the end of the year approaches. The withdrawal of summer reinvestment capital will likely lead to shifts in market dynamics, urging prudent strategies as issuers attempt to manage uncertainty. As the market grapples with these transformations, a keen eye on upcoming elections, potential policy changes, and economic indicators will help shape investment decisions moving forward.

The municipal bond market is undergoing significant changes with evolving yields, fluctuating inflow trends, and increased issuance activity. As investors seek stability amid potential volatility, understanding these dynamics will be crucial in navigating this ever-evolving financial landscape.