Market Trends in Muni Bonds: Insights and Analysis

The municipal bond market is undergoing significant shifts in activity, propelled by various factors affecting yields and investor sentiment. On a recent Thursday, the market witnessed some weakness as new issuances slowed down and municipal mutual funds attracted inflows exceeding $2 billion. Simultaneously, U.S. Treasury yields registered an upward trend beyond five years, which introduced a layer of complexity in the trading atmosphere. The nuances in this market are critical for investors who are trying to navigate both opportunities and challenges.

Yields and Ratios: Understanding Current Metrics

As analyzed through the lens of Municipal Market Data at 3 PM EST, the ratios between municipal bonds and U.S. Treasury yields provide crucial data points for market participants. The two-year ratio was reported at 64%, paralleled by similar metrics for the five-year and ten-year bonds. These figures illustrate the competitive landscape municipal bonds face, not just against Treasuries but also in relation to each other across different maturities. Notably, the thirty-year ratio climbed to 83%, suggesting that long-term investors may find value in longer-dated municipal offerings despite the rising yields.

Kim Olsan, a seasoned fixed-income portfolio manager at NewSquare Capital, noted a curious phenomenon where substantial issuances of high-grade bonds did not repel buyers; in fact, it seemed to bolster confidence in acquiring municipal bonds with attractive yields. This presents a compelling narrative where, even with evident hurdles in supply and demand dynamics—such as lower redemptions and increased issuance—munis are still perceived favorably by investors seeking yield opportunities. The focus, according to Olsan, appears to be on realizing actual returns rather than worrying excessively about the broader market’s supply conditions.

An In-Depth Look at Recent Activities

Analyzing specific transactions offers a glimpse into the robust nature of the municipal market. For instance, Washington State and Nevada’s General Obligation (GO) bonds drew narrowed spreads of +7 to +10/MMD, demonstrating strong demand that typically widens during market downturns. Moreover, AAA-rated issuances from Fairfax County, Virginia, and Mecklenburg County, North Carolina, managed to attract similar narrow spreads or even outperform established benchmarks, showcasing investor confidence.

Olsan also provided insights into a recent auction of A2/A-rated University of Maryland Medical System bonds. The transaction yielded interesting results, with 5-year bonds callable in 2035 priced with respectable spreads compared to averages observed over the previous year. The competitive nature of these bids reflects a prevailing sentiment in the municipal bond sector—investors are keen to capitalize on quality offerings, even when general market conditions might suggest caution.

The secondary market has also demonstrated instructive actions that could signal future trends. Olsan emphasized that the daily trading volume for January is approximately $7.6 billion, representing a significant 30% decrease from the previous year’s average. However, this decline does not correlate to a lack of interest or confidence; rather, it hints at a more selective trading environment where quality over quantity is taking precedence.

Interestingly, January has seen a modest outperformance in both AAA and AA-rated credits, which have rallied several basis points in the ten-year interval. This uptick reflects a desire among investors to gravitate toward secure, high-grade options amid broader uncertainties. It’s telling that combined transactions of AAA and AA bonds encapsulated 85% of market activity, revealing a trend where investors are prioritizing quality.

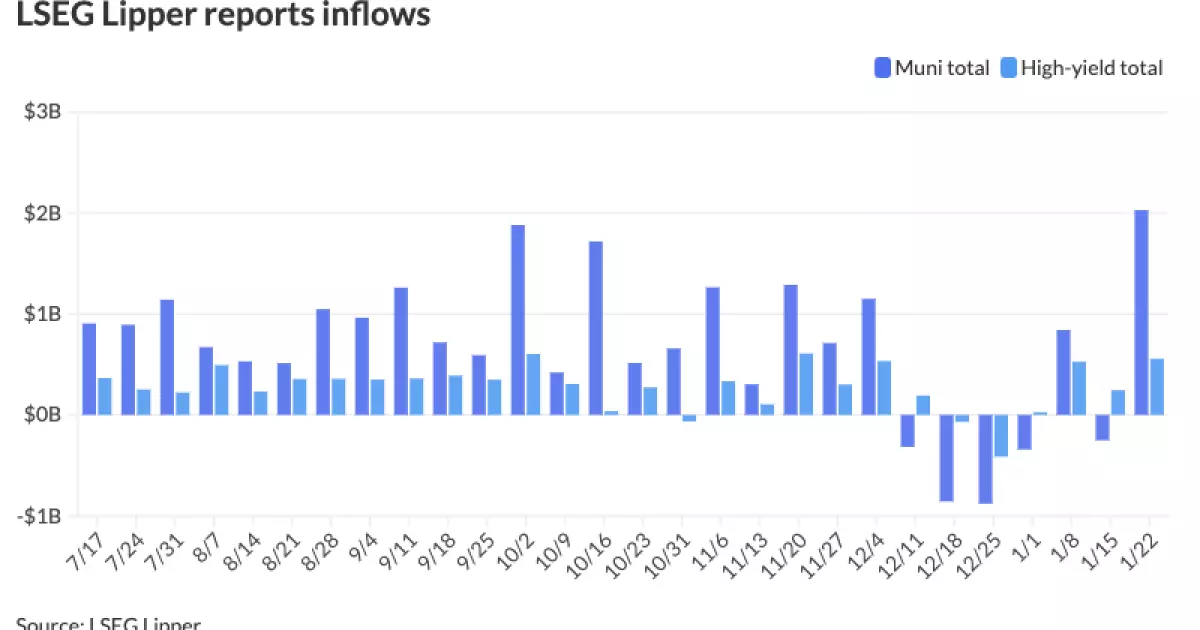

Investor behavior within mutual funds sheds light on underlying market sentiments. Recent data reveals an influx of $2.028 billion into municipal bond mutual funds, contrasting sharply with outflows seen earlier in the month. This marks the largest inflow since January 2023, suggesting renewed investor interest in this asset class. High-yield funds also witnessed increased demand, a positive indicator for risk appetite among municipal bond investors.

Conversely, tax-exempt municipal money market funds faced notable outflows totaling $2.74 billion, which could point to a strategic repositioning by investors seeking greater returns in taxable options. The dynamics here suggest a complex interplay where investors are weighing between riskier opportunities and the safety of high-grade munis.

While the municipal bond market currently faces challenges, including rising yields and fluctuating supply demands, it also offers an array of choices for discerning investors. The capacity to focus on yield and quality amidst changing conditions can lead to beneficial returns. Market participants must remain agile, keeping a keen eye on secondary activities, fund flows, and the overarching macroeconomic landscape to better navigate this evolving space effectively. As evidenced, the appetite for highly rated bonds shows promise, underscoring the enduring appeal of municipal bonds.