Municipal Bond Market: An Unprecedented Surge in 2024

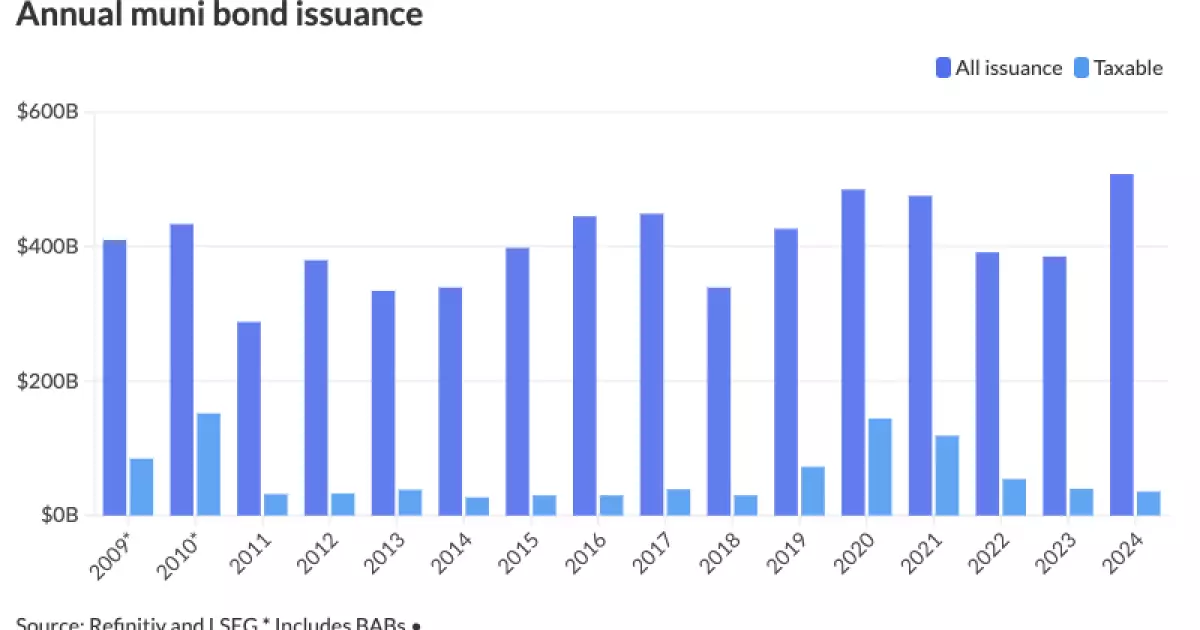

The municipal bond market witnessed a historical rise in 2024, with issuances exceeding $500 billion for the first time. This was fueled by various factors including substantial infrastructure requirements, election-related uncertainties, and an influx of sizable transactions known as “mega deals.” According to LSEG data, the total debt issued reached an impressive $507.585 billion, marking a 31.8% increase from the previous year’s $385.061 billion. This new high not only eclipsed the prior record of $484.601 billion set in 2020 but did so by a significant margin, shedding light on a dynamic market ecosystem responding to both fiscal demands and strategic investments.

The breakdown of issued debt revealed intriguing trends among different types of municipal bonds. Tax-exempt issuance saw a substantial increase of 36%, reaching $446.673 billion from $328.536 billion in 2023. In contrast, taxable issuance experienced a decline of 10.5%, falling from $39.817 billion in 2023 to $35.632 billion in 2024. This juxtaposition illustrates a growing preference for tax-exempt debt in the current financial climate, potentially pointing to heightened government and municipal priorities on accessible funding while navigating economic challenges. Refunding activities also surged by 63.6% to $84.479 billion, signaling an optimization effort among issuers to manage existing debt more favorably.

As 2024 began, market participants expected a progressive increase in issuance after two years of sub-$400 billion totals. Initial forecasts varied widely, suggesting a potential volume range stretching from $330 billion to $450 billion. However, the unexpected strength of the market led many analysts to revise their predictions mid-year. The resurgence was linked to several essential factors, including persistent demand from municipal issuers that were no longer able to rely solely on pandemic-era federal grants and financial assistance.

Kim Olsan, a senior fixed income portfolio manager at NewSquare Capital, noted that the year was characterized by stabilized yields that benefitted both issuers and investors. With higher yields contributing to a more conducive trading environment, there was remarkable engagement from buyers, including exchanges trading funds, even amid a backdrop of market volatility.

The prevailing need for infrastructure investment became a critical driver for municipal bond issuance as federal stimulus funds from previous years dwindled. Chris Brigati, managing director and chief investment officer at SWBC, emphasized the urgency behind this shift; municipalities initially built cash reserves due to available federal funding but now faced the pressing reality of deteriorating infrastructure. There is a pronounced need for upgrades in transportation, healthcare, and education facilities that had grown more acute due to urban expansion, especially in regions like the Southwest and Southeast.

As federal aid diminished, local governments found themselves compelled to turn to the bond market to finance necessary improvements. This pressure to address infrastructure deficits likely contributed to the summer months’ robust issuance figures.

The presidential cycle also influenced issuance patterns, notably in October 2024, which recorded the largest monthly issuance figure at $64.643 billion. As market participants sought to mitigate potential volatility tied to upcoming elections, many issuers strategically accelerated their fundraising efforts. Olsan remarked that uncertainties surrounding the election amplified issuer concerns, driving them to secure financing while conditions were perceived as favorable.

In light of anticipated political change, issuers sought to “lock in” favorable terms and rates, circumventing potential disruption that may arise from electoral outcomes. This implies a reactive strategy within the municipal bond market that aligns closely with broader economic sentiments.

An additional standout feature of the 2024 market was the proliferation of “mega deals,” characterized by bond offerings exceeding the billion-dollar mark. This phenomenological transformation reflects a confidence shift in investors and issuers alike regarding large-scale financing. Olsan noted that large deals were met with positive reception, indicating a fortified appetite among buyers for higher-value offerings. As liquidity trends showed positive correlations with the size of deals, municipal bond issuers were emboldened to explore opportunities that once seemed daunting.

As we look towards 2025, projections indicate that issuance could potentially reach between $480 billion and $745 billion, setting the stage for another significant year. Analysts largely anticipate sustained momentum from 2024, contingent upon several factors, notably interest rates, inflation, and evolving tax policies that may adjust the landscape for public sector financing.

With most forecasts centering around $500 billion, anticipation mounts concerning how governmental bodies will mobilize resources, particularly with impending legislative changes. The ability for issuers to adjust quickly in response will be crucial as they navigate these shifting financial realities.

The municipal bond market in 2024 illustrated a remarkable journey driven by robust issuance, unexpected dynamics in taxable versus tax-exempt segments, and strategic responses to economic and political contexts. As stakeholders reflect on this record-setting year, the momentum continues to build towards 2025, leaving much speculation about future trends and opportunities in municipal finance.